The Organ-on-Chip (OoC), Microfluidics, and New Approach Methodologies (NAMs) space is no longer a niche academic pursuit, it is rapidly becoming a commercial force reshaping how drugs are discovered, toxicology is assessed, and disease is modelled. What was once a handful of pioneering labs has expanded into a dense, competitive ecosystem of startups, scale-ups, and platform companies, each staking out distinct territory across biology, engineering, and data science.

Regulatory tailwinds are accelerating adoption. The FDA Modernization Act 2.0 in the US has opened the door for human-relevant in vitro alternatives to animal testing, and similar momentum is building in the EU. For investors, pharma partners, and drug developers, the question is no longer whether this technology works, it’s which platforms are positioned to win, and where the commercial opportunity is greatest.

This article maps the emerging landscape across key segments, highlighting the companies and leaders driving the space forward.

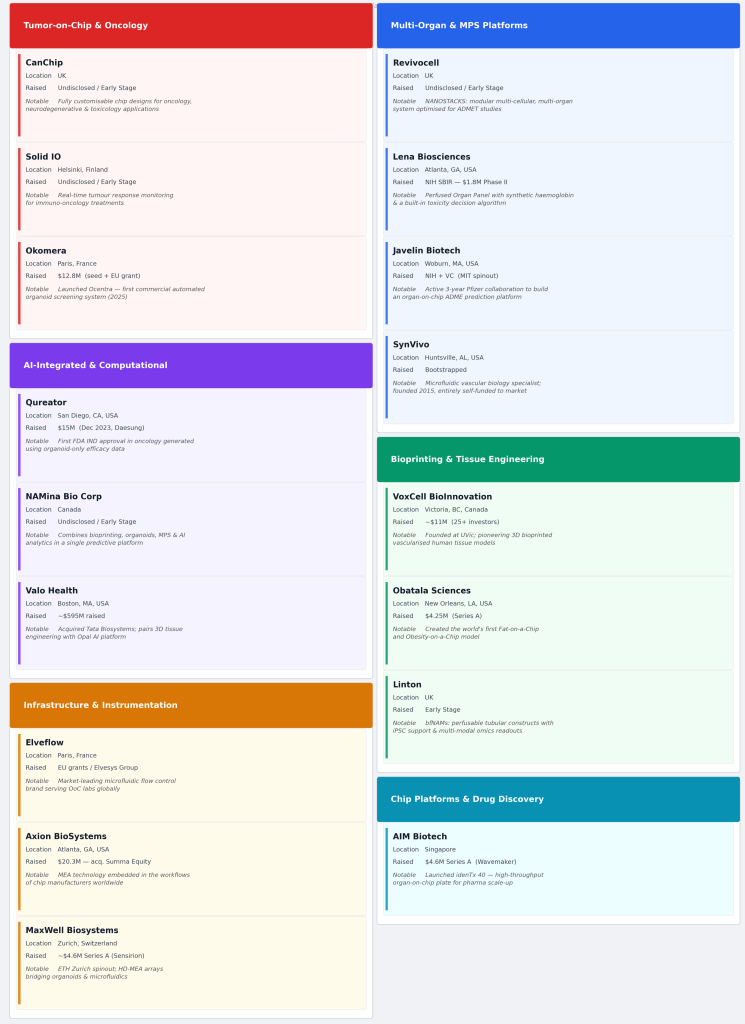

Segment 1: Tumor-on-Chip & Oncology Models

Cancer research is one of the most commercially compelling applications for organ-on-chip technology, where patient-derived models and real-time treatment monitoring can dramatically compress the drug development timeline.

CanChip, led by CEO Ghazaleh Madani, is an early-stage company offering fully customisable Tumor-on-Chip products and services targeting oncology, neurodegenerative disease, and toxicology research. Its customisable approach positions it to serve both academic and pharma clients seeking bespoke model configurations.

Solid IO, founded by Noora Hujala, takes a precision oncology angle — offering real-time insights into how cancers respond to immuno-oncology treatments via its Tumor-on-Chip platform. As immuno-oncology becomes one of the most active areas of pharma R&D spend, platforms that can reliably model tumour-immune dynamics hold significant commercial potential.

Okomera, led by Silvère Lucquin, has developed an automated organoid screening system for 3D patient-derived organoids using microfluidics-on-chip — bridging the gap between high-throughput screening and physiologically relevant 3D biology. Automation is a critical enabler for pharma adoption at scale.

Segment 2: Multi-Organ & Microphysiological Platforms (MPS)

Moving beyond single-organ models, multi-organ microphysiological systems represent the frontier of in vitro biology — enabling researchers to study systemic drug effects across interconnected tissue types.

Revivocell, founded by Valon Llabjani, PhD, has developed the NANOSTACKS system — a multi-cellular, multi-organ in vitro model designed to replicate complex physiological interactions. This category is particularly attractive for ADMET studies, where traditional single-organ models fall short.

Lena Biosciences, led by Jelena Vukasinovic, offers perfused, multi-organ microphysiological platforms that recreate human-like blood flow, oxygen delivery, and tissue environments — a sophisticated approach to modelling the body’s interconnected systems.

Javelin Biotech, under Murat Cirit, has developed a Liver Tissue Chip for preclinical drug testing using MPS models. The liver is the first point of metabolic processing for most drugs, making liver-on-chip models a high-demand product for any pharma company running preclinical safety studies.

SynVivo (Gwen Fewell) rounds out this segment with 3D in vitro models and cell-based microfluidic platforms designed for drug discovery, toxicology, and translational research, with a focus on vascular biology.

Segment 3: AI-Integrated & Computational Disease Models

One of the most significant structural shifts in this space is the convergence of biofabrication with artificial intelligence. Companies integrating computational layers into their biological platforms are positioned to offer not just models, but predictions, a step-change in value for pharma.

Qureator, led by Kyu Baek, combines human disease models with an AI platform that mimics complex disease phenotypes and patient-specific responses, a powerful proposition for personalised medicine and clinical trial design.

NAMina Bio Corp, founded by Paola Dama, integrates 3D bioprinting, organoids, MPS, and AI-powered analytics to build predictive human disease platforms. This multi-modal approach, combining physical models with computational intelligence, reflects where the most sophisticated players in the market are heading.

Valo Health, under Brian Alexander, represents a notable example of vertical integration: its acquisition of Tata Biosystems combined three-dimensional tissue engineering and cardiac disease modelling capabilities with Valo’s proprietary Opal Computational Platform. This kind of deal signals how established computational drug discovery companies view biofabrication as a core capability to own, not merely partner with.

Segment 4: Bioprinting & Tissue Engineering

3D bioprinting is enabling the construction of increasingly complex tissue architectures, including vasculature, the holy grail of tissue engineering, with direct applications in drug testing and eventually therapeutic use.

VoxCell BioInnovation, led by Dr. Karolina Valente, is building vascularised human tissue models using 3D bioprinting to elevate preclinical drug development. Vascularisation has historically been one of the hardest problems in tissue engineering; companies solving it are addressing a genuine bottleneck in the field.

Obatala Sciences, founded by Dr. Trivia Frazier, PhD, MBA, takes a unique niche: using human-derived hydrogels and stem cells to produce its ObaCell Fat-on-a-Chip and Obesity-on-a-Chip models. With metabolic disease representing one of the largest and most underserved areas in drug development, this specialisation is a smart commercial bet.

Linton is building biofabricated New Approach Methodologies (bfNAMs) around a foundational premise: that better medicine depends on better models, and better models must replicate not just the biology of human tissue, but its physical dynamics. The platform focuses on perfusable, tubular tissue constructs that mimic blood vessels and other flow-driven systems — combining biofabrication, biomaterials, and controlled flow environments to capture the haemodynamic and mechanical forces that conventional static in vitro models routinely ignore.

Engineered for versatility across size, geometry, and layer composition — from single-layer constructs to complex multi-layered architectures — the platform is applicable across cardiovascular research, drug delivery, and medical device evaluation. Support for diverse human cell types including iPSC-derived cells enables personalised, multicellular constructs that reflect native tissue complexity. Combined with multiple readout modalities — omics profiling, biosensors, and tissue analysis — Linton’s bfNAMs are designed to serve as a translational validation bridge between in vitro experimentation and clinical reality.

Segment 5: Microfluidics Infrastructure & Instrumentation

Behind every chip and model is an ecosystem of instruments, flow systems, and enabling technology. This infrastructure layer is often underappreciated but critically important, and tends to benefit broadly from growth across the entire sector.

Elveflow Microfluidics (an Elvesys brand), led by Eric Farin, has developed microfluidic flow control and chip solutions specifically for organ-on-a-chip experiments. Infrastructure players like Elveflow operate with a platform business model, they serve the whole market rather than a single application, which can produce durable revenue streams as adoption grows.

Axion BioSystems, under Julien Bradley, enables organ-on-chip experiments by non-invasively monitoring cell activity using multi-electrode array (MEA) technology. Critically, Axion partners with chip manufacturers, a smart positioning that embeds its technology into the workflows of other platform companies, rather than competing with them.

MaxWell Biosystems, led by Urs Frey, offers the MaxOne and MaxTwo systems, acting as a bridge between 3D organoid models and microfluidics. As the field pushes toward more complex 3D models, bridging tools that connect different model types are increasingly valuable.

Segment 6: Chip Platforms & Drug Discovery Services

AIM Biotech, led by Jim McGorry, provides humanised 3D microfluidic platforms and services for drug discovery research. The service model alongside the platform lowers the barrier to adoption for pharma partners who may not want to build in-house capability.

The Bigger Picture: What This Landscape Tells Us

A few structural themes emerge from surveying this ecosystem:

Specialisation is winning over generalism. The most compelling companies have staked out specific disease areas (oncology, metabolic disease, liver toxicity) or specific enabling technologies (MEA monitoring, flow control, bioprinting). The days of claiming to build “an organ-on-a-chip for everything” as a commercial strategy appear to be passing.

AI integration is becoming table stakes. Multiple companies across the landscape are embedding computational intelligence into their platforms. Those that can offer predictive outputs, not just biological data, will command premium positioning with pharma partners.

The infrastructure layer is maturing. The presence of dedicated instrument and flow-control companies signals that the field is past early-stage prototype work and into systematic, reproducible experimentation. This is a classic signal of a market approaching scale.

Leadership diversity is notable. Across this landscape, a striking number of companies are led by diverse scientists and entrepreneurs, a pattern that reflects the academic origins of this technology and one worth recognising as the field enters its commercial phase.

The Microfluidics, Organ-on-Chip, and NAMs market is still in the early chapters of its commercial story. But the density of innovation, the calibre of the founders, and the regulatory direction of travel all point in the same direction: this is a space that will matter significantly to drug development, toxicology, and ultimately patient outcomes over the coming decade.

Leave a comment